Credit cards can be fantastic financial tools when used wisely. They offer convenience, rewards, and security, and help build your credit score. However, they can also become a slippery slope into debt if mismanaged. This guide will walk you through the essentials of using credit cards responsibly, helping you enjoy their benefits while steering clear of financial pitfalls.

Understanding How Credit Cards Work

Credit cards allow you to borrow money from a financial institution to make purchases, with the understanding that you’ll pay it back by a set date. When you use your credit card, you’re essentially taking a short-term loan. If you don’t pay it off in full by the due date, you’ll incur interest charges.

Key Terms to Know:

- Credit Limit: The maximum amount you can borrow on your card.

- Annual Percentage Rate (APR): The interest rate charged on unpaid balances.

- Grace Period: The time between the purchase and the due date, during which no interest is charged if the balance is paid in full.

- Minimum Payment: The smallest amount you can pay to keep your account in good standing.

- Credit Score: A numerical representation of your creditworthiness.

Benefits of Credit Cards

When used properly, credit cards come with numerous advantages, such as:

1. Convenience

Carrying a credit card means you don’t have to carry cash or checks, and it’s widely accepted around the world. Plus, it’s a more secure way to make transactions, both in person and online.

2. Building Credit

Using a credit card and paying your bill on time builds your credit score. A good credit score can help you qualify for better loans, lower interest rates, and even job opportunities, as some employers review credit reports during hiring.

3. Rewards and Cash Back

Many credit cards offer reward programs such as cash back, travel miles, or points that can be redeemed for various products or experiences. If you pay off your balance each month, this is essentially free money.

4. Purchase Protection

Most credit cards offer some form of purchase protection, like extended warranties, fraud protection, and even insurance on certain types of purchases.

Risks of Credit Cards

As convenient as credit cards are, they come with risks that can have serious financial consequences if not managed carefully.

1. High Interest Rates

Credit card interest rates (APRs) are generally higher than other types of loans. If you carry a balance month to month, you could end up paying much more for purchases due to interest charges.

2. Temptation to Overspend

It’s easy to overspend when you’re not physically handing over money. Credit cards can give a false sense of security, leading to spending beyond your means.

3. Credit Score Damage

Missing payments or carrying high balances can damage your credit score. A poor credit score can make it more difficult to qualify for loans or favorable interest rates in the future.

4. Debt Cycle

If you’re not careful, it’s easy to fall into a cycle of paying only the minimum payment, which means you’re primarily paying off interest rather than the principal balance. This can lead to accumulating debt that becomes hard to pay off.

How to Use Credit Cards Wisely

The good news is that with some discipline and knowledge, you can use your credit cards to your advantage and avoid debt. Here are some strategies to help you do just that:

1. Pay Your Balance in Full

To avoid paying interest, always aim to pay your credit card bill in full each month. If you can’t, pay as much as you can to reduce interest charges.

2. Create a Budget

Treat your credit card like cash. Before making purchases, ensure they’re within your budget. Track your spending regularly to avoid surprises when your bill arrives.

3. Set Up Auto Payments

To avoid missing due dates, set up automatic payments for at least the minimum payment. Better yet, schedule full payments if your budget allows.

4. Avoid Unnecessary Purchases

Don’t let rewards programs tempt you into buying things you don’t need. The cashback or points you earn won’t be worth it if you’re carrying a balance and paying interest.

5. Monitor Your Credit Utilization Ratio

Try to keep your credit utilization (the amount you owe compared to your credit limit) below 30%. High credit utilization can lower your credit score.

6. Review Your Statements

Regularly review your credit card statements for any unauthorized charges or errors. Report any suspicious activity immediately to your credit card provider.

7. Limit the Number of Cards

While it may be tempting to have multiple credit cards for different rewards, juggling too many accounts can make it difficult to manage payments and could lead to debt.

What to Do if You’re Already in Debt

If you’ve already accumulated credit card debt, don’t panic. Here are steps you can take to start digging yourself out:

1. Stop Using Your Credit Cards

First, halt all new spending on your credit cards until you get the balance under control. Focus on cash or debit card purchases for now.

2. Pay More Than the Minimum

Making only the minimum payment will barely chip away at your balance, as most of it goes to interest. Instead, pay as much as you can each month.

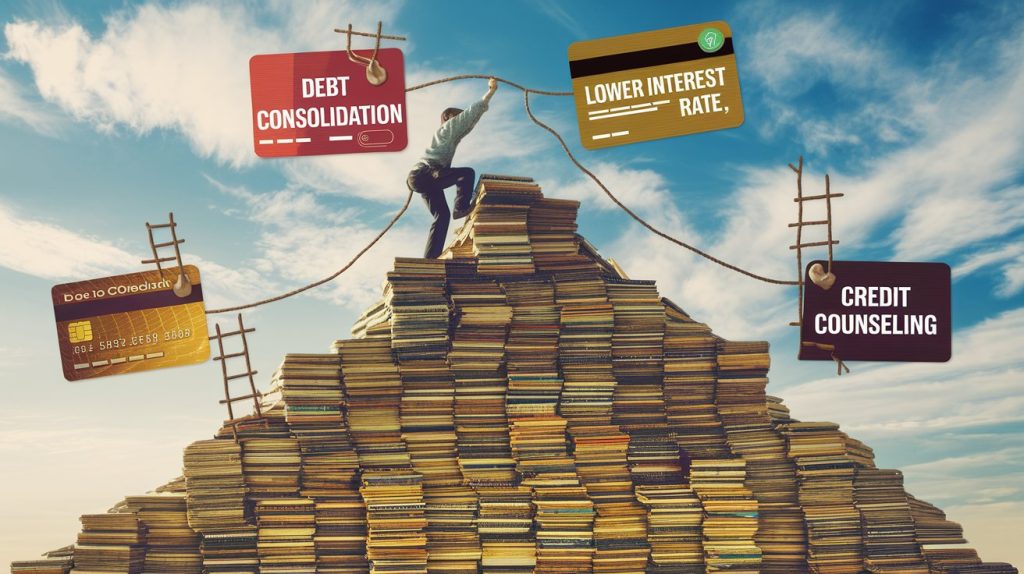

3. Negotiate a Lower Interest Rate

Call your credit card company and ask for a lower interest rate. You’d be surprised how often creditors are willing to lower rates, especially if you’ve been a good customer.

4. Consolidate Your Debt

If you have debt on multiple cards, consider consolidating it into one loan with a lower interest rate. Many banks offer balance transfer cards with 0% APR for an introductory period, allowing you to pay off your balance faster.

5. Seek Professional Help

If you’re overwhelmed, consider reaching out to a credit counselor or a debt relief service. They can help create a debt management plan tailored to your situation.

Conclusion

Credit cards can be incredibly useful, offering convenience, rewards, and credit-building potential. But without careful management, they can also lead to debt and financial stress. By understanding how credit cards work and using them wisely, you can enjoy the benefits without falling into the traps.

Remember, the key to managing credit cards responsibly is to treat them as a tool, not free money. Spend within your means, pay off your balance each month, and always keep an eye on your budget. By following these steps, you’ll be on the path to financial success without the burden of credit card debt.

You can also read Understanding Credit Scores and How to Improve Yours.